Saturday, February 16, 2013

Climate Push 2013: A Cold-Eyed Look at Sanders-Boxer

Although it has a zero chance of getting past a Republican veto in congress, it’s good to see a new climate bill sponsored by Bernie Sanders and Barbara Boxer. You need a concrete proposal to transform amorphous climate anxiety into political activism. The fate of this bill will have little to do with its actual strengths and weaknesses, but we should still size it up carefully, since politics often has a way of digging channels that it eventually has to follow.

In some ways this is an evolutionary improvement on Waxman-Markey, which made it through the House in 2009 but died in the Senate. Like W-M, its centerpiece is a framework for putting a price on carbon, a sine qua non for organizing a comprehensive response to the buildup of greenhouse gases. Unlike W-M, it would position itself upstream, slapping a tax on fossil fuels as they leave the ground or enter the economy from abroad. This is a huge improvement: it would cover a wider swath of carbon emissions and would avoid all the loopholes and backroom dealing that sector-by-sector coverage practically invites.

Also, it devotes three-fifths of all carbon revenues to per capita rebates back to the public. This is essential for several reasons: it is good macroeconomics (more predictable muting of the dampening effect of higher energy costs), good social policy (turning regressive fuel price increases into progressive redistribution), and good politics (countering the understandable fear of households that rising energy bills will slash their living standards). This is the right direction for policy.

The brief summary posted on Sanders’ website doesn’t make clear how long or complex the bill is, but from the looks of it, it should be simpler and more transparent than W-M. That’s important too.

However, there’s another possible comparison to make: Maria Cantwell’s CLEAR Act. This was introduced at the same time as W-M but didn’t get the endorsement of either the Democratic Party establishment or the major green groups. It was a much, much better approach.

Rather than collecting money through a tax, CLEAR required permits to introduce fossil fuels into the economy, and these permits would be auctioned. Permits have two large advantages over taxes. First, the relationship between carbon prices and emissions is uncertain and likely to change over time. By setting one, you allow the other to fluctuate. If you are a climate hawk—and you should be—you want the price to vary and to control directly how much carbon we send up into the atmosphere. Permits do this. Second, as a practical matter, it will be difficult to pass a bill that does more than impose a token restriction on carbon emissions, at least initially. S-B, for instance, starts low at $20 per ton of CO2 equivalent and programs a very modest rate of increase over the next decade. In fact, it anticipates only a 20% reduction in emissions by 2025, not nearly what we need. By itself, that’s OK; just getting a framework is a big deal. But basing the framework on taxes means that, if we somehow manage to make S-B the law of the land, we are going to have to spend the next decade arguing for higher taxes on fossil fuels. That’s tough not only because of the politics of taxes, but also because taxes are connected to climate outcomes only through a chain of effects that is complex and imprecise. It would be much more powerful, politically, to be arguing about how much carbon to send up to the atmosphere directly, which is what you get from a permit system. There’s a reason Bill McKibben’s outfit is named 350.org and not, say, $120-per-ton.org.

Also, CLEAR rebated nearly all of its revenues back to the public. Rebating some of the money is a good idea, and the more you rebate the better it is. That way you cover more of the public’s fears about energy costs, recycle more of the cost increases into other forms of demand, etc. Ah, you say, but what about all the investments in clean energy we need to make? Yes, we need to make them, but we don’t need any extra revenue: we could finance them almost entirely out of repurposing anti-environmental spending on fossil fuel subsidies, ag subsidies, a large portion of military spending, and so on. You can even see that, camouflaged, in S-B. It proposes to increase green investments of all sorts by $480B over ten years, along with ending fossil fuel subsidies—but then it would devote $300B of these savings (from ending subsidies) to reducing fiscal deficits. In other words, the majority of the money that could have gone into rebates is going into financing the government—and this is based on just one of many possible changes in federal spending. It is important to bear in mind that price increases for energy are highly regressive in themselves; so programming a more austere fiscal policy at the expense of lower income households is a double no-no.

So there you are: we have a new starting point that’s better than the “official” proposal last time around but worse than its better competitor. The good and bad news is that we will have lots of time—at least two years and probably longer—to discuss what the best framework would look like.

Thursday, February 14, 2013

Open The Doors To Immigrant Physicians!

Since I recently poked at my friend, Dean Baker, let me agree with him strongly on a recent post of his dealing with an important issue widely ignored, the need to relax our strict immigration rules for physicians. It is widely agreed that the major threat to future US fiscal solvency is the rising cost of medical care. US physicians are paid on average $250,000 per year, more than twice what European ones are, and simply higher than any others in the world. If salaries were to fall to European levels, we would save $100 billion per year in medical costs. However, neither political party is pushing this, and it is rarely discussed among the many ideas that get put forward regarding controlling medical care costs. Almost certainly this reflects the power of the AMA with both political parties.

A sign of this ignoring is a recent NY Times article on STEM immigration that Dean links to. He very reasonably points out how there is no mention of the physician issue, and indeed the US has a shortage of physicians, particularly of primary care ones. He has also long complained about high income professionals such as doctors and lawyers being for free trade, but imposing immigration restrictions on potential competitors for themselves. For more discussion, see http://www.cepr.net/index.php/blogs/beat-the-press/why-arent-they-talking-about-immigrant-doctors .

A sign of this ignoring is a recent NY Times article on STEM immigration that Dean links to. He very reasonably points out how there is no mention of the physician issue, and indeed the US has a shortage of physicians, particularly of primary care ones. He has also long complained about high income professionals such as doctors and lawyers being for free trade, but imposing immigration restrictions on potential competitors for themselves. For more discussion, see http://www.cepr.net/index.php/blogs/beat-the-press/why-arent-they-talking-about-immigrant-doctors .

Monday, February 11, 2013

Is Dean Baker Wrong About Robert J. Samuelson On the S&P Prosecution?

I am usually in agreement with Dean Baker and jumping up and down on the case of Robert J. Samuelson of the Washington Post. However, in this case of Dean dumping on Samuelson for raising questions about the recently announced DOJ case against the S&P ratings agency for fraud back prior to the 2008 collapse, see http://www.cepr.net/index.php/blogs/beat-the-press/robert-samuelson-is-worried-the-justice-department-is-persecuting-sap , I am not fully in agreement with Dean. Dean accurately points out that all parties involved were convinced that the real estate bubble was going to continue, but that fraud may still have occurred as the S&P raters may have changed their business model and were rating derivatives and CDOs as AAA without any solid support.

So, why I am defending the often indefensible RJS? It is not because of any argument that he made. The problems are two in my view. One of them, mentioned by RJS, is that this is awfully long after the alleged crime (which indeed I think happened) to be finally be getting around to this. The other, more important and not noted by either of them, is that this is the only ratings agency to be so prosecuted, with a very large fine being requested, one large enough to trigger a bankruptcy of S&P's parent company, McGraw-Hill. Why is S&P the only one so charged? What sticks out to me is that S&P was the agency that downgraded the US debt rating after the debt ceiling in 2011, much to the annoyance of the administration at the time.

I happen to agree that this was somewhat questionable and obnoxious, although the breakdown of responsible decisionmaking in Washington was certainly something worthy of criticism, and it certainly was not illegal of S&P to make such a downgrade. But there is all together too much scuttlebutt that this prosecution is in fact in response to this particular action by S&P. They are being singled out among the various probably guilty ratings agencies for punishment possibly because they did something that annoyed the administration on policy grounds. This is arbitrary action that strikes me as being an inappropriate way to proceed. Either punish all of them, or none of them, and if punishing, then do it sooner after the alleged crime in question. This smells of a political payback.

So, why I am defending the often indefensible RJS? It is not because of any argument that he made. The problems are two in my view. One of them, mentioned by RJS, is that this is awfully long after the alleged crime (which indeed I think happened) to be finally be getting around to this. The other, more important and not noted by either of them, is that this is the only ratings agency to be so prosecuted, with a very large fine being requested, one large enough to trigger a bankruptcy of S&P's parent company, McGraw-Hill. Why is S&P the only one so charged? What sticks out to me is that S&P was the agency that downgraded the US debt rating after the debt ceiling in 2011, much to the annoyance of the administration at the time.

I happen to agree that this was somewhat questionable and obnoxious, although the breakdown of responsible decisionmaking in Washington was certainly something worthy of criticism, and it certainly was not illegal of S&P to make such a downgrade. But there is all together too much scuttlebutt that this prosecution is in fact in response to this particular action by S&P. They are being singled out among the various probably guilty ratings agencies for punishment possibly because they did something that annoyed the administration on policy grounds. This is arbitrary action that strikes me as being an inappropriate way to proceed. Either punish all of them, or none of them, and if punishing, then do it sooner after the alleged crime in question. This smells of a political payback.

Why Aren’t Corporations Paying More in Dividends and Does It Matter to Aggregate Demand?

Tyler Cowen likely regrets writing this about Paul Krugman’s observation that corporations are hoarding a lot of cash:

I would understand it (though not quite accept it) if corporations were stashing currency in the cupboard. Instead, it seems that large corporations invest the money as quickly as possible. It can be put in the bank and then lent out. It can purchase commercial paper, which boosts investment. Maybe you are less impressed if say Apple buys T-Bills, but still the funds are recirculated quickly to other investors. This may not end in a dazzling burst of growth, but there is no unique problem associated with the first round of where the funds come from. If there is a problem, it is because no one sees especially attractive investment opportunities in great quantity. (To the extent there is a real desire to invest, the Coase theorem will get the money there.) That’s a problem at varying levels of corporate profits and some call it The Great Stagnation. The same response holds if Apple puts the money into banks which earn IOR at the Fed and the money “simply sits there.” The corporations are not withholding this money from the loanable funds market but rather, to the extent there is a problem, the loanable funds market does not know how to invest it at a sufficiently high ROR.If anything, large corporations are more likely to diversify out of the U.S. dollar, which could boost our exports a bit, a plus for a Keynesian or liquidity trap story.Paul and Peter Dorman suggest Tyler is committing Say’s Fallacy (also known as Say’s Law which basically ignores the possibility of insufficient aggregate demand). As Peter puts it:

The problem is not that corporate money can’t find its way to ultimate investment, but that too much corporate money itself reduces the pull of final demand on the level of investment. The upshot isn’t that money disappears into cupboards, but that national income is lower than it would otherwise be.I was going to add my two cents with the first one being on why corporations would be hoarding cash – but then Noah Smith has done a fine job on that query. To throw in my other cent – let me temporarily don the hat of a Barro-Ricardian equivalence type. Suppose that shareholders were all very rational agents with no borrowing constraints and that they recognized that all this hoarded cash was their wealth. Whether the corporation issued dividends or not, their wealth is unaffected. So maybe these households would be consuming the profits be they hoarded in cash or issued out in dividends. Now I know this equivalence theorem does not necessarily hold up that well in the real world so we can talk about tax cuts stimulating consumption for at least households that do face borrowing constraints. We liberals therefore tend to argue that tax cuts for the working poor tend to have a larger direct effect on aggregate demand than tax cuts for the ultrarich. So if the shareholder were someone who was borrowing constrained, hoarding cash rather than paying dividends does depress consumption demand. Then again – we liberals also tend to argue that a lot of shareholder wealth is owned by very rich individuals as opposed to being owned by the working poor. Non-Ricardians are welcome to tell me where this line of thinking has gone terribly astray!

Sunday, February 10, 2013

The Difficulty of Thinking Macroeconomically, Exhibit C: Tyler Cowen and the Corporate Cash Hoard

Paul Krugman worries about the macro implications of corporations scarfing up unprecedented profits while sitting on a hoard of liquid assets. Tyler Cowen doesn’t understand why:

I am confused by this argument. I would understand it (though not quite accept it) if corporations were stashing currency in the cupboard. Instead, it seems that large corporations invest the money as quickly as possible. It can be put in the bank and then lent out. It can purchase commercial paper, which boosts investment....If there is a problem, it is because no one sees especially attractive investment opportunities in great quantity.Ah, but why are these investment opportunities lacking? Could one of the reasons be that too high a fraction of national income is being funneled into corporate profits, rather than households inclined to spend it? What Cowen has trouble with is seeing all the pieces simultaneously in true macro fashion. The problem is not that corporate money can’t find its way to ultimate investment, but that too much corporate money itself reduces the pull of final demand on the level of investment. The upshot isn’t that money disappears into cupboards, but that national income is lower than it would otherwise be.

I’m sympathetic with Cowen’s struggle: I see the same difficulties in my economics classes every year. Students can usually see only one or two linkages at a time; it is really hard to see the whole thing as one simultaneous entity. It doesn’t come easy even for professional economists, since writing a set of equations is one thing, but visualizing them on an intuitive level as an integrated system is another.

The fact is, there are a lot more Tyler Cowen’s in this world than Paul Krugman’s, which is one reason why it is so difficult to get a sensible discussion of macroeconomic policy.

Saturday, February 9, 2013

Risk = Freedom?

There’s a review on the Dissent website by Steve Randy Waldman of Freaks of Fortune: The Emerging World of Capitalism and Risk in America by Jonathan Levy. The book sounds interesting, but it is apparently based on a commonplace but false understanding of the relationship between freedom and risk-taking.

At the individual level it is absolutely true that we face a tradeoff between risk and freedom. You can opt for a secure life, but only at the expense of creativity, individualism, moral courage and all the other Emersonian goodies. Each one of us, every day, faces this choice. Mostly it is just a matter of a tiny bit of risk-taking, but these moments add up, and from time to time there is a fundamental fork in the road. We make our own freedom.

But the social level is another story. Individuals take the array of risks as given; society can choose how much risk its members will face and what their risk-freedom tradeoffs will be, at least up to a point. If the objective is to minimize all risk of any sort, especially all risks to health and income, the result will be stultifying. But that’s not where we are on the Great Risk Curve. Rather, the debates we have are about whether to cut back or extend social insurance programs like Social Security and Medicare, social protections like TANF and Medicaid, and more or less regulation of finance, pollution and such. It seems clear to me that more security of this sort, which limits the downside risk individuals face in their personal lives, reduces the cost of living freely.

Examples are everywhere. Ample unemployment insurance makes it easier to work for a startup or switch jobs in general rather than being held down by too strong a need for job security. A stronger public pension system encourages entrepreneurship: people can hazard their savings by starting a business rather than hoarding everything for old age. Social guarantees for basic needs make it possible for artists to risk making art their day job. Professors with tenure (big time risk reduction) can take more controversial positions on public issues. (I don’t say they always do this, but they do it more than they would if all professors were temps.) In each case there is a real tradeoff between freedom and security at the individual level, but society can create programs that relax it, so it takes less courage to live freely.

That’s what I don’t like about the nanny state rhetoric. Yes, of course the state can go too far and overprotect us from risks we would do better to face ourselves. But the state we actually live in goes too far in the other direction. With a stronger safety net we could have less risk and more freedom.

Wednesday, February 6, 2013

The Myth Of The Money Multiplier

Something unusal happened yesterday in my weekly department macroeconomics seminar at James Madison University. Someone had us discuss a paper that changed the minds of pretty much everybody in the room who did not already agree with the paper, which includes a highly diverse group ranging from Austrian, Old Monetarist, New Classical, New Keynesian, Old Keynesian, Post Keynesian, and some generally eclectic pragmatists. The paper is from the Fed Bd of Govs in 2010, by Seth Carpenter and Selva Demiralp, still unpublished as near as I can tell, and is entitled, "Money, Reserves, and the Transmission of Monetary Policy: Does the Money Multiplier Exist?" Their answer is not only "no," which I at least have thought was true since 2007 or so, but that the answer has been "no" probably since the mid-1980s and certainly since the mid-1990s. It is available at http://www.federalreserve.gov/pubs/feds/2010/201041/201041pap.pdf .

The story can be seen pretty much in figures and charts in the back. Prior to 1984, there was a clear correlation between reserves, loans, and M2. After then, while loans and M2 continued to go along in a pretty close lockstep, reserves simply have flopped around all over the place. This seems to have coincided with various things: a definite move to targeting interest rates and apparently following a Taylor rule (although not more recently on the latter), the change in Regulation Q, globalization, a broadening of sources of funds for banks, and particularly more interbank lending and lessening of reliance on reserves and the Fed's reserve base. Apparently up to the mid-90s, small umdercapitalized banks still were tied to reserves in their lending, but after then that broke down too, with their appearing to be a shift to relying more on large deposits, mostly from other banks and also the shadow banking system.

That Fed control over the money supply has become a phantom has been quite clear since the Minsky moment in 2008, with the Fed massively expanding its balance sheet without much resulting increase in measured money supply. This of course has made a hash of all the people ranting about the Fed "printing money," which presumably will lead to hyperinflation any minute (eeek!). But the deeper story that some of us were unaware of is that apparently this disjuncture happened a long time ago. Even so, one of our number pointed out that official Fed literature and even many Fed employees still sell the reserve base story tied to a money multiplier to the public, just as one continues to find it in the textbooks, But apparently most of them know better, and the money multiplier became a myth a long time ago.

Barkley Rosser

The story can be seen pretty much in figures and charts in the back. Prior to 1984, there was a clear correlation between reserves, loans, and M2. After then, while loans and M2 continued to go along in a pretty close lockstep, reserves simply have flopped around all over the place. This seems to have coincided with various things: a definite move to targeting interest rates and apparently following a Taylor rule (although not more recently on the latter), the change in Regulation Q, globalization, a broadening of sources of funds for banks, and particularly more interbank lending and lessening of reliance on reserves and the Fed's reserve base. Apparently up to the mid-90s, small umdercapitalized banks still were tied to reserves in their lending, but after then that broke down too, with their appearing to be a shift to relying more on large deposits, mostly from other banks and also the shadow banking system.

That Fed control over the money supply has become a phantom has been quite clear since the Minsky moment in 2008, with the Fed massively expanding its balance sheet without much resulting increase in measured money supply. This of course has made a hash of all the people ranting about the Fed "printing money," which presumably will lead to hyperinflation any minute (eeek!). But the deeper story that some of us were unaware of is that apparently this disjuncture happened a long time ago. Even so, one of our number pointed out that official Fed literature and even many Fed employees still sell the reserve base story tied to a money multiplier to the public, just as one continues to find it in the textbooks, But apparently most of them know better, and the money multiplier became a myth a long time ago.

Barkley Rosser

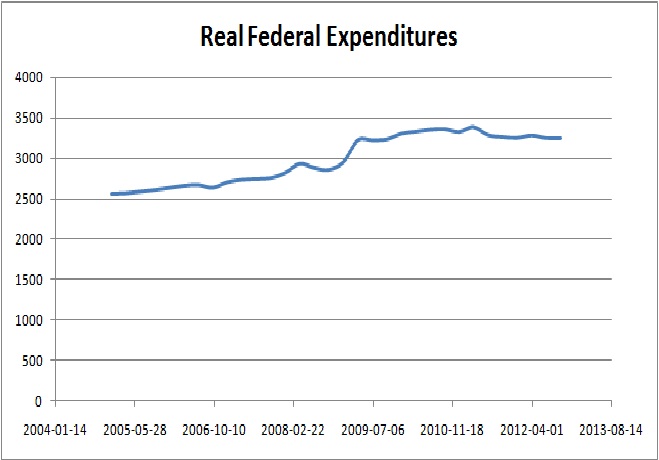

Real Federal Expenditures

There was no decrease in government spending during the fourth quarter of last year. In fact, the government spent more money between October and December of 2012 than it did during the previous two quarters. So federal spending actually increased during the 4th quarter.Nolte was complaining about how some claimed there was a fall in government spending reported in the latest GDP accounts. Of course, people should distinguish between government purchases (which did fall in real terms last quarter) and government spending which includes transfer payments as Barkley noted. But let’s make two other distinctions. My post yesterday linked to Federal expenditures on a seasonally adjusted basis which did show a sizeable decline even in nominal terms between the 2nd and 3rd quarter and a nominal increase that was less than inflation in the 4th quarter. So in real terms, seasonally adjusted real Federal expenditures have fallen during the second half of 2012. In fact, they have been falling since their peak at the end of 2010. Perhaps part of the decline is attributable to the fact that the economy has slowly recovered but part of it is due to austerity, which of course, is terrible policy for an economy that still has a 6% GDP gap. And some in Congress want to cut government spending even more?

Tuesday, February 5, 2013

Federal Expenditures – Seasonally Adjusted

John Nolte thinks he understands government spending data but I’m not so sure:

There was no decrease in government spending during the fourth quarter of last year. In fact, the government spent more money between October and December of 2012 than it did during the previous two quarters. So federal spending actually increased during the 4th quarter. Would you like some facts to go with your media propaganda?Barkley helped clear up some of Nolte’s confusion:

What may be a problem here is that the public reports did not make this distinction, reporting on declines in "government spending," when in fact what is involved here has been a decline in government purchases. The crucial issue here is that changes in transfer payments do not directly affect GDP, but changes in government purchases do, and it was purchases, mostly through defense spending, that declined.But we should also note that Nolte presented Federal outlay data which exhibits seasonality. Which is why the government accounts also present the data with seasonal adjustments. Nolte’s observations don’t quite hold when we look at Federal spending seasonally adjusted.

A Humorous Lesson in Financial Etymology

Public disgust with bankers is nothing new. In the fifteenth and

sixteenth century the most powerful banking family, which took over much

of power and influence of the Medicis. Their name, Fugger, became a

slang word associated with rapacious behavior.

Monday, February 4, 2013

Government Purchases Versus Government Spending

It is interesting that PGL has posted a figure showing government purchases and how they have been gradually declining recently. The recent report of GDP surprisingly declining in fourth quarter 2012 and the role of government spending in that brings this up. What may be a problem here is that the public reports did not make this distinction, reporting on declines in "government spending," when in fact what is involved here has been a decline in government purchases. The crucial issue here is that changes in transfer payments do not directly affect GDP, but changes in government purchases do, and it was purchases, mostly through defense spending, that declined.

Some readers may say, "What is the problem here?" The problem is that a new right wing meme has erupted over whether or not "government spending" has declined. Indeed, it did not do so during the 4th quarter 2012, at least not federal government spending. Much as I dislike this source, one can see the numbers taken from US Treasury stats at http://www.breitbart.com/Big-Government/2013/01/30/Fact-Check-Federal-Spending-Increased-in-4th-Quarter .

Furthermore, Barron's has gotten all huffy about how the Bureau of Economic Analysis reported the decline in defense spending, which indeed was mostly a decline in purchases leading to a decline in GDP. They complain that the 22% reported number for the quarterly decline was an annualized number, and that the actual decline was only 5.32%. This is accurate, but indeed, that decline in purchases by the DOD happened and was unexpected (although following a sharp increase in the 3rd quarter, thought by many to be a forwarding of spending in anticipation of the fiscal cliff/sequester/etc.) and played a major role in the reported GDP quarterly decline.

In any case, the increase in federal spending noted by Breitbart was due to an increase in transfer payments that did not lead to an increase in GDP. As it is, people should be warned that this meme is now out there. I became aware of it when I saw the editorial page lead editorial in my very conservative hometown Harrisonburg (VA) Daily News-Record, which was going on about the government lying and Obama lying and so on and so forth, all on the basis of this report that in fact government spending had gone up rather than gone down as the media so widely reported. It would have been helpful if the original reports on this had been a bit clearer, although I suspect that much of the public is simply unaware of the distinction here or its importance.

Meanwhile, everyone should keep in mind that the much bigger story here has been the ongoing decline in state and local government spending and purchases, with a far larger proportion of their spending being in fact purchases. Their employment is also much higher than that of the federal government, just over 19 million in comparison with about 4.4 million for the federal government, the latter peaking in recent decades at about 5.3 million in 1987 and reaching a recent minimum in 2000 of about 4.1 million. Since peaking in August 2008, government employment has fallen more than 700,000, with the overwhelming majority of that being in the state and local sector, with that decline still occurring in the last job report, where the gain of 157,000 jobs was after a 9000 jobs loss in the government sector, again, mostly state and local. Federal employment has not changed much in this whole period, increasing some in 2009 and slightly decreasing since, although that could change if there continue to be substantial declines of federal government purchases.

Barkley Rosser

Some readers may say, "What is the problem here?" The problem is that a new right wing meme has erupted over whether or not "government spending" has declined. Indeed, it did not do so during the 4th quarter 2012, at least not federal government spending. Much as I dislike this source, one can see the numbers taken from US Treasury stats at http://www.breitbart.com/Big-Government/2013/01/30/Fact-Check-Federal-Spending-Increased-in-4th-Quarter .

Furthermore, Barron's has gotten all huffy about how the Bureau of Economic Analysis reported the decline in defense spending, which indeed was mostly a decline in purchases leading to a decline in GDP. They complain that the 22% reported number for the quarterly decline was an annualized number, and that the actual decline was only 5.32%. This is accurate, but indeed, that decline in purchases by the DOD happened and was unexpected (although following a sharp increase in the 3rd quarter, thought by many to be a forwarding of spending in anticipation of the fiscal cliff/sequester/etc.) and played a major role in the reported GDP quarterly decline.

In any case, the increase in federal spending noted by Breitbart was due to an increase in transfer payments that did not lead to an increase in GDP. As it is, people should be warned that this meme is now out there. I became aware of it when I saw the editorial page lead editorial in my very conservative hometown Harrisonburg (VA) Daily News-Record, which was going on about the government lying and Obama lying and so on and so forth, all on the basis of this report that in fact government spending had gone up rather than gone down as the media so widely reported. It would have been helpful if the original reports on this had been a bit clearer, although I suspect that much of the public is simply unaware of the distinction here or its importance.

Meanwhile, everyone should keep in mind that the much bigger story here has been the ongoing decline in state and local government spending and purchases, with a far larger proportion of their spending being in fact purchases. Their employment is also much higher than that of the federal government, just over 19 million in comparison with about 4.4 million for the federal government, the latter peaking in recent decades at about 5.3 million in 1987 and reaching a recent minimum in 2000 of about 4.1 million. Since peaking in August 2008, government employment has fallen more than 700,000, with the overwhelming majority of that being in the state and local sector, with that decline still occurring in the last job report, where the gain of 157,000 jobs was after a 9000 jobs loss in the government sector, again, mostly state and local. Federal employment has not changed much in this whole period, increasing some in 2009 and slightly decreasing since, although that could change if there continue to be substantial declines of federal government purchases.

Barkley Rosser

Does Paul Ryan Know What Austerity Means?

I didn’t see Meet the Press, and there doesn’t seem to be a transcript available yes, but I hear that Paul Ryan declared it a proven fact that Keynesian economics has failed — and was, of course, not challenged on that assertion.Since Krugman has already challenged any assertion that Keynesian economics failed, let me pick up the pieces and show the key part of the MTP exchange:

GREGORY: Yeah, I know. A lot of centrist economists who may disagree with you in some areas but agree about the imposing or the impending debt crisis. Some on the left like Paul Krugman disagree. He calls you a deficit scold and he calls you worse than that. But his point is that-- that you’re being alarmist about the deficit and its relationship to how the economy performs and how the economy grows. So here’s what he wrote in his column on Friday and let me get you to respond to it. “It was, in fact, a good thing that the deficit was allowed to rise as the economy slumped. With private spending plunging as the housing bubble popped and cash-strapped families cut back, the willingness of the government to keep spending was one of the main reasons we didn’t experience a full replay of the Great Depression.” And this balance now between austerity, which he believes you call for, and appropriate investment on the part of the government is still where the great tension is. REP. RYAN: Well, we can debate the efficacy of changing economics or not and I don’t obviously believe-- I think that that is pretty clear, it doesn’t work. We’re not preaching austerity. We’re preaching growth and opportunity. What we are saying is if you get our fiscal shift fixed, you preempt austerity. That’s the-- here’s what a debt crisis is. A debt crisis is what they have in Europe, which is austerity. You cut the safety net immediately. You cut retirement benefits for people who’ve already retired. You raised tax and slow down the economy, young people don’t have jobs. That’s the austerity that comes when you have a debt crisis. And when you keep stacking up trillion dollar deficits like this government is doing, it’s bringing us to that moment. Our job, our goal is to prevent and preempt austerity so we can get back to growth.I guess it took MTP a week to post this transcript given how incredibly embarrassing it really is. Let’s start with the fact that we have been cutting government purchases (austerity) for the past couple of years, which is a major reason why the recovery has basically stalled. But Ryan is calling for more government spending cuts so we can avoid austerity? Does this alleged GOP economic guru even know what the word austerity means?

Sunday, February 3, 2013

The S-Word

A question thrown my way yesterday got me thinking about what my views are on socialism today. (They keep changing.) Here is a quick summary, more for getting my thoughts in order than to satisfy whatever interest there may be out there in blogland.

1. Objectives. There are four areas in which capitalism often falls short and which might be served better by fundamental economic change.

a. A poor balance of intrinsic and extrinsic motivation. For me, extrinsic motivation is a precise way to characterize psychological alienation. A world in which people are motivated to live their lives as intrinsically as possible is, all else equal, offers a better, more meaningful way of life. Of course, lots of important activities can’t be reliably left to intrinsic motivation, so this is not an all-or-nothing issue. It seems clear to me, however, that we could have a much better balance than we now see. Of course, intrinsic motivation is also linked to other issues, like the perceived fairness of the organizations we take part in and the reasonableness of what these organizations do.

b. Equality. For an egalitarian like me, more economic and social equality is better, again all else equal. Equal doesn’t mean “same”, of course. We will continue to live, as we should, in a highly differentiated world, but it doesn’t have to be so hierarchical. As with motivation, there are practical tradeoffs to take into consideration with equality; whether or not we face a tradeoff today between greater collective prosperity and greater equality (probably not), as equality is increased such a tradeoff must inevitably appear. But to say that absolutely perfect equality is unattainable is not to say that we couldn’t thrive in a much more equal world.

c. Social control over economic life. It is essential that our economic activities, which, as technology develops, become ever more far-reaching in their effects, be subjected to broad social control. As a starting point, however, it is important to recognize that the market can quite often serve as a perfectly adequate mechanism of such control. To take an example, think about the problem of producing shoes for a population with a wide variety of foot shapes and sizes. I believe the market does a creditable job of generating and distributing an assortment of shoes that meet this collective need for diversity, both statically (existing technology) and dynamically (encouraging an appropriate level of effort in the development of new technologies for making footwear production more flexible). This is a matter of some interest to me, because I have oddly-shaped feet. (Note that I’m restricting the issue to the problem of foot diversity, not to the different question of whether everyone who needs some sort of footwear can get it.) On the other end of the spectrum, the market is doing a terrible job of propelling us into a desperately-needed transition to carbon-free energy, with all it entails for infrastructure, residential and commercial location, patterns of consumption, and other related matters. Arguably, there are many other, if perhaps less pressing, aspects of economic life that call out for greater social direction.

In connection with this point, it should be mentioned that there are two interrelated dimensions to social control. First, this entails the formation of the “social” itself, the achievement of we-ness, jointness of purpose, in a society of (ideally) free individuals. I certainly don’t expect that we would or even should arrive at a monolithic unity at the level of society as a whole; a desirable social-ness would be a mosaic of cross-cutting social groups, with individuals experiencing multiple affiliations. You might consider this an extension of Tocqueville’s observations on association or Dewey’s reflections on democracy as a way of life. It sounds rather airy and abstract but takes very practical, material form in the social institutions we create or could create in the ordinary course of life. The second element is “control”, which, the closer you look at it, the more slippery it becomes. As I’ve written elsewhere, ownership does not determine control in the modern world; control is multifaceted and inheres at all levels of economic life, from the most granular (a work team) to the most systemic (like a market). Social control suggests something like a stakeholder economy, but with a much more developed, encompassing and democratically constituted set of stakeholders and a variety of mechanisms that incorporate them at all levels of the system, as is practical and meaningful. But not too many meetings, please: the resources for democracy are limited and should be allocated to their most important uses.

d. Class politics. When I’m feeling optimistic, I can imagine all the problems of capitalism being fixed by incremental tweaking, except one, the overweening power of the capitalist class. A system of private ownership undertaken for profit cannot avoid creating a small group, a 1% of the 1%, who command an outsized portion of society’s wealth and can use it in a variety of ways to influence the political process. One reason it is difficult to make progress on the preceding issues is the grossly disproportionate power of this minuscule group. Nearly every proposal for circumscribing this power has been adopted somewhere on the planet, but no country has managed to actually tame it. This may be the single negative feature of capitalism least amenable to reform.

In principle, I identify socialism with progress on these four fronts and not with any particular institutional forms.

2. Reform versus system change. This topic may be mislabeled: I’m not convinced that it is justified to think of potential economies as discrete systems, boxes that are separated from one another by hard walls. Nevertheless, there is a crucial strategic decision to make: do we prefer to make small, incremental changes in economic institutions or large, multiple changes all at once? (This is about preference, but sometimes our preferences don’t matter: there may be no alternative to piecemeal or systemwide change under the historical conditions we find ourselves in.)

Here are the arguments for incremental reform:

a. Economic, political and social life are unimaginably complex, and our knowledge of how they work is spotty and often in error. In order to avoid unintended outcomes, we should take small steps, learning as much as possible along the way from our successes and failures. This is the logic of adaptive management.

b. Small steps usually entail less conflict and especially less violent conflict. Violent conflict is bad for three reasons: it is harmful in itself, it results in chaotic situations whose outcomes are difficult to predict and control, and it typically institutes a dynamic of repression and exclusion that poisons the forms of democratic participation that a desirable socialism requires.

There are also two general arguments for radical, systemwide change.

a. Because of the interconnectedness between elements of the economic system, it may be the case that multiple, simultaneous changes are feasible while piecemeal changes are not. This is an application to social change of the logic of interactive nonconvexity.

b. One possible lesson of history is that opportunities for significant change come infrequently and should be used to their fullest. Reformism might be the right strategy in a world of open, democratically responsive politics, but that is not the world we live in. Change should push up against its political limits and not be self-limiting.

As you can see, these are not finished propositions but ways of framing questions. In fact, I would distrust any set of answers that are held to apply in every situation we might find ourselves in.

Thursday, January 31, 2013

GDP Gap Stuck at 6%

A sharp drop in government spending, heavily concentrated in defense, coupled with a decline in inventories caused GDP to shrink at a 0.1 percent rate in the 4th quarter. Government spending fell at a 6.6 percent annual rate, driven by a 22.2 percent decline in defense spending, subtracting 1.33 percentage points from the growth rate in the quarter. A 40.3 drop in the rate of inventory accumulation reduced growth by another 1.27 percentage points. Without these factors, GDP would have grown at a 2.5 percent annual rate in the quarter. Pulling out these extraordinary factors, the GDP data were largely in line with prior quarters.Inventory changes often turn out to be transitory events while I have faith that those military Keynesians in the Republican Party will push for more defense spending pork. But let’s be clear about what is going on with the GDP gap. While it did fall from 7.5% in mid 2009 to around 6% at the end of 2010, it has been basically stuck at 6% ever since. So recent GDP growth has been insufficient. Dean also rightfully turns on our fiscal policy prospects:

There is little evidence in this report to believe that the economy will diverge sharply from a 2.5- 3.0 percent growth path, except for the impact of the deficit reductions that Congress is considering or already put in place. Higher tax collections from the ending of the payroll tax holiday are likely to knock around 0.5 percentage points from growth. The sequester, or whatever cuts are put in place in lieu of the sequester, are likely to have an even larger impact on growth beginning in the second quarter.Fiscal austerity has been a large part of the reason why we have been stuck at a 6% GDP gap. Many economists have been strongly recommending fiscal stimulus but I guess our political leaders choose not to listen.

Tuesday, January 29, 2013

Joe Scarborough on the Deficit

After his interview with Paul Krugman this morning Joe Scarborough wrote:

Mr. Krugman's view is that Americans would be better off if its government ran deeper deficits and ignored its longterm debt.To suggest that Keynesians like Paul Krugman ignore the long-term government budget constraint is either dishonest or shows that Mr. Scarborough does not understand what we are saying. Which is why Mr. Scarborough should check out this list of commentary on the current economics and fiscal situation compiled by Joe Weisenthal.

Subscribe to:

Comments (Atom)