I must congratulate Heritage Action on their principled move to "score" votes of US Senators on the confirmation of Janet Yellen to become Chair of the Board of Governors of the US Federal Reserve System. They are doing this in order to register their protest against the "politicization" of the Fed and to fight against it. Surely, there is no better way to depoliticize the Fed than to threaten any Senator (particularly a GOP one) with facing a well-funded teabag opponent in a primary if they dare to vote for the appointment of Yellen. I must applaud Heritage Action on its sagacity and wisdom in this move (hack, cough)...

Barkley Rosser

Friday, November 29, 2013

Tuesday, November 26, 2013

Bibi And GOP Whine While Stock Market and Spooks Love Iran Nuke Deal

Yesterday the Wall Street Journal top headline told us that there was much opposition to the Iran nuclear deal that Sec. State John Kerry has pulled off with Iran and the P5+1 in Geneva. Israeli PM Bibi Netanyahu is loudly denouncing it as a horrible mistake, and many Republkicans in Congress are joining in with his denunciation, despite 2 to 1 public opinion poll support in the US.

However, it looks like Bibi is out of step with some important opinion makers in Israel itself on this matter, who seem to view the matter in a much more favorable light. One is the Israeli stock market, reaching new highs in the wake of the agreement, and more silently but there nevertheless, the Israeli military-intelligence security establishment, whom Bibi likes to ignore in order to enflame his political backers and undercut Obama, whom he is very annoyed he failed to have Romney defeat last year in the US election, darn it!

Sorry. Bad links; for the second one, try . The one I linked to is Stratfor that does not get it and still thinks the Saudis are upset. They are not. For the first one, there are lots of sources out there about the Israeli stock market booming on the news.

Barkley Rosser

However, it looks like Bibi is out of step with some important opinion makers in Israel itself on this matter, who seem to view the matter in a much more favorable light. One is the Israeli stock market, reaching new highs in the wake of the agreement, and more silently but there nevertheless, the Israeli military-intelligence security establishment, whom Bibi likes to ignore in order to enflame his political backers and undercut Obama, whom he is very annoyed he failed to have Romney defeat last year in the US election, darn it!

Sorry. Bad links; for the second one, try . The one I linked to is Stratfor that does not get it and still thinks the Saudis are upset. They are not. For the first one, there are lots of sources out there about the Israeli stock market booming on the news.

Barkley Rosser

Monday, November 25, 2013

Dean Baker v. Greg Mankiw on Wage Inflation

I may have been too nice to Greg Mankiw per something Dean Baker notes with support from Paul Krugman. Dean notes:

if we use the broader measure of wage growth for all workers, we don't see any evidence of acceleration at all. Wage growth has been hovering around 2.0 percent for the last two and a half years. It had been somewhat lower in 2010 (@ 1.6 percent), but there certainly is no upward pattern in this series.Paul adds:

One of these numbers, wages of production and nonsupervisory workers, shows a modest uptick, the others not. All three remain well below their pre-crisis rates of increase. Is this the kind of evidence on which you want to base a major policy change? Not in my world.Whether we examine the growth in average hourly earnings for production and nonsupervisory workers, the growth in average hourly earnings for all employees, or the employment cost index, wages seem to be rising by only 2% per year. If this increase in nominal wages is matched by an increase in productivity, one would think that unit labor costs would not be rising. The Bureau of Labor Statistics publishes the change in unit labor costs on a national basis every quarter. Unit labor costs actually fell by 3.7% in 2010 and have barely increased since. Call me old school – but why are we worried about a modest increase in nominal wages when unit labor costs are basically flat?

Sunday, November 24, 2013

Former Romney Economic Advisors on the State of the Labor Market

While the Washington Republican leaders keep pushing austerity and complain about the Federal Reserve pursuing expansionary monetary policy, it is refreshing to see what Greg Mankiw is saying about the choices Janet Yellen will have to face:

In her recent testimony before the Senate Banking Committee, Janet L. Yellen, the eminently qualified nominee to lead the Fed, made clear she didn’t think the time for an exit had come. With inflation running below the Fed target of 2 percent and continued weakness in the labor market, she argued, the economy needs all the help the central bank can provide. Many of the numbers back up that diagnosis.Mankiw note only cites the continuing high unemployment rate but also the low employment to population rate. Yet, Mankiw did note some contrary evidence:

Seven years ago, the vacancy rate was a bit over 3 percent. It fell to a low of 1.6 percent in July 2009, a month after the official trough of the recession. The most recent reading puts it at 2.8 percent. So according to this measure of labor-market tightness, the economy is almost back to normal. Data on wage inflation also suggest that the labor market has firmed up. Over the past year, average hourly earnings of production and nonsupervisory employees grew 2.2 percent, compared with 1.3 percent in the previous 12 months. Accelerating wage growth is not the sign of a deeply depressed labor market.John Taylor, however, thinks the labor market is still incredibly weak:

Research by Christopher Erceg and Andrew Levin is providing solid evidence that the decline in the labor force participation rate since 2007 has been due to cyclical factors–the recession and slow recovery–rather than to demographic factors. In other words, the fact that such a large number of people have dropped out of the labor force is associated with the weak economy rather than to their reaching their retirement years–or some other typical demographic trend. Because the unemployment rate does not count the people who dropped out of the labor force it no longer gives a good reading of the state of the labor market. The unemployment rate would be much higher without this large decline in labor force participation.Taylor shows the Erceg-Levin chart with unemployment adjusted for a “normal” labor force participation rate, which suggests an adjusted rate near 11%. He concludes:

There is no longer debate that the labor market performance in this recovery–and the recovery itself–is unusually weak. The debate is now over why. I have argued that it is the economic policy.This is all fine but he didn’t say what economic policy should be doing. Does he still believe that Quantitative Easing should have been discontinued three years ago?

Friday, November 22, 2013

Minimum Wages and Macroeconomic Silliness

Mark Perry has a silly argument against raising the minimum wage, which thankfully David Cooper has ably addressed. The gist of Perry’s argument is captured by his title:

In Western Europe, the average jobless rate is twice as high in countries with a minimum wage vs. those with no minimumCooper replies:

First of all, as we learned in Statistics 101, there’s a difference between correlation and causation. Even if there appeared to be some pattern between minimum wages and unemployment, that wouldn’t mean that one is in any way causing the other. The only way to try to identify causality is to isolate as many—ideally all—other factors that might play a role in the suspected relationship through statistical regression methods … take a look at the countries that do have minimum wages. If minimum wage laws do lead to higher joblessness, as Perry suggests, one would expect that the higher the minimum wage, the higher the jobless rate. According to this table, that’s not the case in Western Europe. The figure below is a simple scatterplot of the minimum wage rates and the jobless rates from the table. As you can see, under the superficial approach that Dr. Perry is viewing these data, higher minimum wages actually imply lower jobless rates.Note that Greece’s minimum wage is quite low and it has a 27.2% unemployment rate. On the other hand, Luxembourg has a very high minimum wage but its unemployment is quite modest. If we are playing this game, we could also look at the real minimum wage in the U.S. over time comparing it to our unemployment rate. After all – the real minimum wage peaked in 1968, which was also a year where the unemployment rate dropped to 3.4%. David Cooper is not suggesting that higher minimum wages tend to lower unemployment rate, but we are saying that Dr. Perry’s little exercise is silly.

Thursday, November 21, 2013

Taylor Rule Follow-up: Core CPI Is Not Biased

Paul Krugman made a valuable contribution on measuring inflation in light of my post on the latest from John Taylor:

Or at least it seems to be a new rule — namely, pick whatever price index makes the point you want, even if it’s not at all the price index you would normally use … Um, the inflation rate for the “GDP price index”? That’s the GDP deflator, which the Fed very carefully does not use as a policy indicator. Why? Because it contains things like grain and oil prices, which fluctuate a lot, so that it’s an unstable measure that is highly unreliable as an indicator of underlying inflation. The Fed prefers the consumption deflator excluding food and energy.Taylor has a heated reply but alas it is all heat and no light:

Rather than taking out food and energy price inflation I controlled for price volatility in that rule by averaging overall inflation over time. Simply taking out food and energy price inflation can lead to policy errors especially when such inflation lasts for more than a short time. And it is not only the overall GDP price level. The CPI inflation rate was also rising, not falling, during this period. In any case, the increase rather than a decrease in overall inflation was only one part of my assessment that this was not a slack period. I also discussed the unemployment rate—which got quite low (4.4%) rather than high as in slack periods—and the huge housing boom with high housing price inflation.OK – inflation rose but only slightly. A 4.4% unemployment rate was certainly not low in comparison to what we witnessed in the late 1990’s. And it is odd that Dr. Taylor refused to acknowledge my point that the FED had already been increasing interest rates before the labor market got moderately over the Bush recession. As far as the housing boom – which President Bush used to brag about – a lot of the blame should go to unwise financial market deregulation – but I guess it would be political suicide for a Republican economist to acknowledge that. In my view, Krugman reader JCB had a more interesting – albeit invalid (as I will explain) – set of comments:

Does eliminating the most volatile categories of consumer expenditure such as food, energy, and home prices from the calculation of the year-on-year rate of inflation make it possible to ignore them as important elements of the long term standard of living? I mean, why tacitly assume that the most volatile prices will sum to zero in the long run? ... The cumulative divergence between all-consumer prices and "underlying inflation" increases between 2000-2013JCB provided us with his evidence, which was a chart showing how core CPI rose by a cumulative amount of 32% over the 2000 to 2013 period whereas CPI (including food and energy) rose by a cumulative amount of 38% during this same period. This period has often been described as the great commodities boom as noted by Pedro Conceição and Heloisa Marone:

{kind=link}

The trough, since when the 21st century boom started, took place in late 2001. In real terms (using the US CPI to deflate the nominal price series), the boom remains impressive, with indices more than doubling in real terms. However, real prices were still below the average prices of the 1970s and earlier decades (Figure 2).If one compared core CPI to overall CPI for the period from 1979 to 2001, core CPI rose faster than the overall consumer price index. Over the entire period, both series have increased by about 228%. If JCB was trying to suggest a long-term bias in the use of core CPI, I don’t see it. Rather – I just see more volatility in the use of an index that includes food and energy prices.

Monday, November 18, 2013

John Taylor on Monetary Policy and Inflation

If you were expecting John Taylor to address what Barry Ritholtz noted about that 2010 prediction of inflation, stop holding your breath. Taylor instead tried a rebuttal to the latest from Lawrence Summers. Taylor’s summary of Summer’s argument starts with this:

In the years before the crisis and recession, easy money and related regulatory policies should have shown up in demand pressures, rising inflation, and boom-like conditions. But the economy failed to overheat and there was significant slack.Taylor of late has been saying that our current mess was created by a deviation from the Taylor rule. Here’s his evidence:

Inflation was not steady or falling during the easy money period from 2003-2005. It was rising. During the years from 2003 to 2005, when Fed’s interest rate was too low, the inflation rate for the GDP price index doubled from 1.7% to 3.4% per year. On top of that there was an extraordinary inflation and boom in the housing market as demand for homes skyrocketed and home price inflation took off, exacerbated by the low interest rate and regulatory policy. Finally, the unemployment rate got as low as 4.4% well below the natural rate, not a sign of slack.Wow – hyperinflation! No one during the Bush Administration – its advisors (which included Taylor) nor its critics – were saying back then that the employment to population ratio had become dangerously high. The 4.4% unemployment rate – which corresponds to a 63.4% employment to population ratio – was not reached until late 2006. By then, we had seen two years of rising short-term interest rates. Now had Taylor and his fellow Bush economic advisors were very concerned about excessive aggregate demand – why did we not seen calls for fiscal restraint back then? If Taylor thinks this is a serious rebuttal to what Summers said, it is no surprise he has yet to acknowledge that 2010 forecast of inflation from QE.

Saturday, November 16, 2013

The Consol Solution To The Debt Ceiling Crisis

Yeah, I know. It is not currently a crisis. That is Obamacare, blah blah blah. But that website will get fixed and those who lost their crappy insurance policies will get them extended, blah blah blah. The remaining serious crisis that could still plunge the world economy into a massive economic plunge, even with the very wise and capable Janet Yellen at the helm of the US Fed, would be a US default on its debt following a failure to raise the debt ceiling in time, with the most likely scenario for this being increasingly delusional Congressional GOPsters out to destroy the economy so they can get elected blaming it all on socialist Obamacare, blah blah blah. Probably wise heads, or at least not completely delusional ones, will prevail, but the fury and delusions in the weird sub-media bubble of the teabags seems to be intensifying.

Now quite a few of us, including such folks as Bill Clinton, Bruce Bartlett, me, and a lot of others, have said that how Barack Obama should deal with this once and for all for all future presidents and the US and world economies, is to declare this motherfucker of a debt ceiling unconstitutional, which it is, even if a GOP dominated SCOTUS might disagree. But one of them might realize the threat and support reason on it, if faced with the prospect of a massive global economic collapse as bad as anything ever seen. In any case, Obama has not followed our advice, and given that he pulled off the latest crisis with only the most minor of market blips may be making him complacent, as well as his enemies, who likewise given the lack of market fear (for once ratex worked; they forecast the ceiling would be raised and it was), may not be held back and may take us over the brink. It is much more likely than most today think.

So, in yesterday's (Nov. 15) Washington Post in its Friday forum, there is an innovative and interesting column on this issue by James Leitner and Ian Shapiro, "A new tool to avert a debt crisis," and I completely agree with them and wish to publicize this alternative tool to those that Obama has rejected (there is also the goofy trillion dollar platinum coin alternative, which both the Treasury and Fed have publicly declared they will not go along with). This solution is to issue consols if the Congress foolishly refuses to raise the debt ceiling in the nest round of this silliness coming up early next year.

The column taught me things I did not know. The term "consol" is short for "consolidated," and sometime in the 1700s the UK consolidated a bunch of long-term bonds. Then in the 1800s they began to issue the actual consols, bonds with infinite maturity, public "annuities" if you will. They just pay interest forever. Quite a few were issued in the heyday of British domination of the world economy in the Pax Brittanica of 1815-1914. Some were retired, but according to Leitner and Shapiro some still exist in the UK government portfolio, still paying their interest. Of course in fin econ textbooks they are the real world example for that nice simple back of the envelope formula that is also relevant for real estate that says that PV = NR/r, where PV is present value, NR is a constant real net return forever, and r is the real interest rate or discount rate for this most basic of present value calculations.

Anyway, Leitner and Shapiro point out a curious detail of how the US legally measures the national debt: only bonds with finite maturities add to it. So, if the debt ceiling is hit, the US Treasury could issue consols that will not legally add to the national debt. The US Treasury will be able to continue to borrow money and pay bills and avoid defaulting while not legally adding to the national debt.

OK OK, there is a dark side, and I give them credit for recognizing it. These consols may require higher interest rates than other US government securities, in violation of the usual pattern that longer term securities provide lower yields. They suggest that if Obama is forced to issue these at higher than usual interest rates he publicize how much these are costing taxpayers and blame it publicly and loudly on the reprobate Congresstrolls. The only further thing they suggest is that the Treasury get at issuing a few soon to get a target interest rate and prepare everybody. I completely agree.

Now quite a few of us, including such folks as Bill Clinton, Bruce Bartlett, me, and a lot of others, have said that how Barack Obama should deal with this once and for all for all future presidents and the US and world economies, is to declare this motherfucker of a debt ceiling unconstitutional, which it is, even if a GOP dominated SCOTUS might disagree. But one of them might realize the threat and support reason on it, if faced with the prospect of a massive global economic collapse as bad as anything ever seen. In any case, Obama has not followed our advice, and given that he pulled off the latest crisis with only the most minor of market blips may be making him complacent, as well as his enemies, who likewise given the lack of market fear (for once ratex worked; they forecast the ceiling would be raised and it was), may not be held back and may take us over the brink. It is much more likely than most today think.

So, in yesterday's (Nov. 15) Washington Post in its Friday forum, there is an innovative and interesting column on this issue by James Leitner and Ian Shapiro, "A new tool to avert a debt crisis," and I completely agree with them and wish to publicize this alternative tool to those that Obama has rejected (there is also the goofy trillion dollar platinum coin alternative, which both the Treasury and Fed have publicly declared they will not go along with). This solution is to issue consols if the Congress foolishly refuses to raise the debt ceiling in the nest round of this silliness coming up early next year.

The column taught me things I did not know. The term "consol" is short for "consolidated," and sometime in the 1700s the UK consolidated a bunch of long-term bonds. Then in the 1800s they began to issue the actual consols, bonds with infinite maturity, public "annuities" if you will. They just pay interest forever. Quite a few were issued in the heyday of British domination of the world economy in the Pax Brittanica of 1815-1914. Some were retired, but according to Leitner and Shapiro some still exist in the UK government portfolio, still paying their interest. Of course in fin econ textbooks they are the real world example for that nice simple back of the envelope formula that is also relevant for real estate that says that PV = NR/r, where PV is present value, NR is a constant real net return forever, and r is the real interest rate or discount rate for this most basic of present value calculations.

Anyway, Leitner and Shapiro point out a curious detail of how the US legally measures the national debt: only bonds with finite maturities add to it. So, if the debt ceiling is hit, the US Treasury could issue consols that will not legally add to the national debt. The US Treasury will be able to continue to borrow money and pay bills and avoid defaulting while not legally adding to the national debt.

OK OK, there is a dark side, and I give them credit for recognizing it. These consols may require higher interest rates than other US government securities, in violation of the usual pattern that longer term securities provide lower yields. They suggest that if Obama is forced to issue these at higher than usual interest rates he publicize how much these are costing taxpayers and blame it publicly and loudly on the reprobate Congresstrolls. The only further thing they suggest is that the Treasury get at issuing a few soon to get a target interest rate and prepare everybody. I completely agree.

Monday, November 11, 2013

State & LocalAusterity – Is Christie Doing His Job?

New Jersey Gov. Chris Christie (R) went on four morning talk shows on Sunday to tout his sweeping re-election victory as a model for the Republican Party nationwide, but the prospective 2016 presidential contender carefully refrained from staking a position on contentious issues such as immigration reform and deliberations over Iran's nuclear program. Throughout the morning, Christie left the door open for a 2016 presidential run while making it clear that governing New Jersey is his focus right now.Christie has also been talking tough about doing his job and being honest with citizens. I’m happy to focus on New Jersey issues but first let me express my only frustration ever with the excellent posts from Bill McBride who suggests state & local austerity is over:

Now state and local governments have added to GDP for two consecutive quarters, and I expect state and local governments to continue to make small positive contributions to GDP going forward.State and local government purchases have inched up for the past two quarters but only after a sustained period of decline. To be fair to Bill – his graph of government employment dates back for over a decade showing how deep the state and local government austerity has been. Governor Christie campaigned very dishonestly on the claim that he balanced the budget and had incredible employment growth. In truth, the New Jersey employment record sort of tracked the national record. At the end of 2007, employment was 4.3 million but dropped to 4.1 million by mid-2009. Its recovery has brought this figure only back to 4.2 million as of August 2013. In other words, employment is still 2.3% shy of where it was before the Great Recession. Nationally, employment is only 1.1% shy of where it was before the Great Recession. I say “only” here but you might protest that employment would have had to grow by almost 5.7% in order to get back to the old employment to population ratio. Christie was asked about this point from the Wall Street Journal:

Among the headwinds for the Republican as he sets an agenda for 2014: a state unemployment rate of 8.5% in August, compared with 7.3% nationally (and among the 10 highest of all states); a slower recovery from the recession compared with the nation; and a budget with a slimmer surplus than those in most of the rest of the country.One of his responses was that New Jersey has created 144,000 new private sector jobs. Of course, that figure used as its starting point the bottom of the employment decline. But then how can I claim that total employment rose by only 100,000 new jobs since the bottom? Could it be that government employment was reduced by around 40,000 during Christie’s tenure in office? In other words, Christie sees his job as fiscal austerity which only makes the employment situation worse. And yet he brags about how he has somehow improved New Jersey’s employment situation? I guess the press thinks this is honest because Christie shouts when he says this nonsense.

Sunday, November 10, 2013

Job Market Doldrums Continue

The news of 204 thousand extra jobs should be treated carefully. Nobody should be excited (assuming, of course, that anything in economics can be exciting). What really demands our attention is the changes that occur from year to year. After all, month-to-month numbers can involve all sorts of temporary changes that indicate nothing about the trend. So looking at the increase in employment from October 2012 to October 2013, the number is 194 thousand per month, which is slightly less exciting than 204 thousand.

More importantly, even though by this measure job creation has been rising since early 2013, the October-to-October increase in hiring was significantly slower than what we saw in early 2012. Job creation may catch up with what happened then, but when the demand for products is growing slowly that also means bad conditions for job-seekers. (According to the Bureau of Economic Analysis of the U.S. Department of Commerce, real GDP grew only 2.8% in the third quarter. It’s likely to turn out to be worse than that, once we see more accurate estimates. GDP must increase more than about 3% for an entire year to truly lower unemployment rate.)

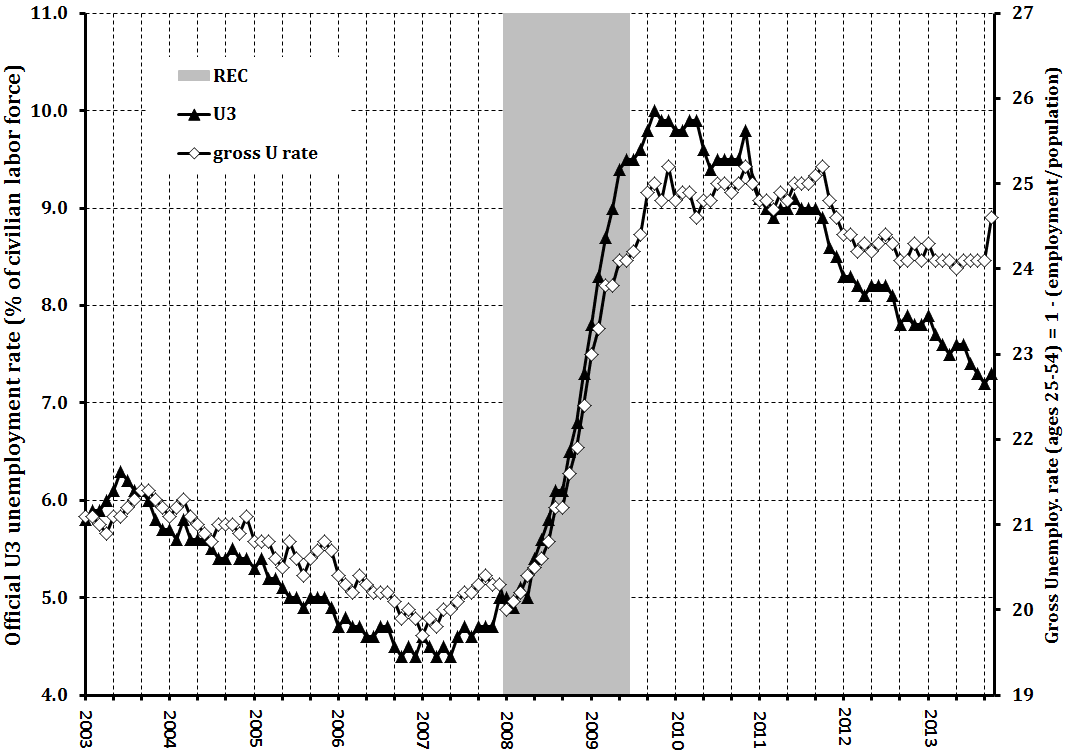

Even more importantly, the unemployment situation has not been improving much at all. U.S. labor markets cannot be said to have recovered from the "Great Recession" of 2008-2009. As the graph shows, it's true that the official (U3) unemployment rate has edged downward since early 201. At its height, it was at 10% and now it's down to 7.3%. This is still high by most economists' standards.

As anyone who's studied macroeconomic should know, this number misses the fact that a lot of unemployment people can -- and do -- stop being counted as unemployed by the BLS if they stop actively looking for jobs. And that kind of discouragement can hit in a big way if the job market is miserable month after month. The most likely to be discouraged from further job-seeking are the long-term unemployed (which the BLS defines as those who have jobless for a half year or more) was about 4.1 million in October, about 36% of the unemployed. Again, if these folks stop looking for jobs, they're no longer counted as unemployed.

To correct for this effect, I calculated the "gross unemployment rate." It's simply a reflection of the employment/population ratio that labor economists often use to help figure out what’s going one but it's designed to be easy to compare to the official U3 rate. (My ratio is simply 100% minus that e-pop ratio). Note that the one I calculated this time is only for people between the ages of 25 and 54, so it doesn't reflect retirements or college graduation very much if at all.)

The gross unemployment rate mostly moves in step with the official unemployment rate. This is seen most dramatically during the Great Recession (the gray stripe in the graph). But in its stagnant aftermath, notice that my gross unemployment rate has generally stayed high, being about 24% in 2013. The improvements in these numbers occurred in the past, i.e., during 2011 and early 2012.

Notice also that if we look at the gross unemployment rate, the numbers jumped in October. It's only a one month leap, but it reflects the government's temporary shut-down. The fact that it rose much more than the official rate reflects the way that a lot of people have stopped looking for jobs. It’s quite possible that this event will continue to keep the growth of GDP slow. Of course, it could just be a one-time event that will be reversed. -- Jim Devine

Saturday, November 9, 2013

Last Call: The Unconventional PetroleuMLM Pyramid

Robert Litterman, a former partner at Goldman Sachs and co-developer of the Black-Litterman Portfolio Allocation Model, argued this week that divestment from fossil fuel companies makes economic sense:

Update: At New Scientist, Jeremy Leggett agrees "An oil crash is on its way and we should be ready":

Perhaps. But as I reflect on Canadian government policy promoting pipelines and tar sands development and industry hype about tight oil and shale gas I get another impression: fraud. Equity markets are not merely failing to build in expectations about climate risk; they are being gamed. They are being gamed by policy manipulation at the highest levels. The unconvential "carbon bubble," as Lee and Ellis call it, is not just a bubble but is THE bubble -- successor to the housing bubble that was the successor to the dot.com bubble. It is a policy-induced pyramid, a Ponzi scheme and a multi-level marketing scam all rolled up into one.

The "last call" in a tavern is also a marketing opportunity. The customers may even load up on more drinks then they might otherwise order. After all, what the heck, it's... closing time.

and I lift my glass to the Awful Truth

which you can't reveal to the Ears of Youth

except to say it isn't worth a dime

And the whole damn place goes crazy twice

and it's once for the devil and once for Christ

but the Boss don't like these dizzy heights

we're busted in the blinding lights,

busted in the blinding lights

of CLOSING TIME

It is well known that emissions markets have not yet priced climate risk appropriately, but what is not well understood is that today’s equity markets build in expectations that climate risk will not be priced rationally for a very long time. The market expects a slow increase in emissions prices over the next several decades. But what the market does not yet realize is that this expectation, sometimes referred to as the “slow policy ramp,” is irrational — it does not appropriately take risk into account.Back in March, Marc Lee and Brock Ellis of the Canadian Centre for Policy Alternatives presented a similar, much more detailed analysis of the financial risk of stranded assets arising from "irrational" pricing of carbon emissions that ignores climate reality.

Update: At New Scientist, Jeremy Leggett agrees "An oil crash is on its way and we should be ready":

It is because of the sheer prevalence of risk blindness, overlain with the pervasiveness of oil dependency in modern economies, that I conclude system collapse is probably inevitable within a few years.So much for "rational expectations"?

Perhaps. But as I reflect on Canadian government policy promoting pipelines and tar sands development and industry hype about tight oil and shale gas I get another impression: fraud. Equity markets are not merely failing to build in expectations about climate risk; they are being gamed. They are being gamed by policy manipulation at the highest levels. The unconvential "carbon bubble," as Lee and Ellis call it, is not just a bubble but is THE bubble -- successor to the housing bubble that was the successor to the dot.com bubble. It is a policy-induced pyramid, a Ponzi scheme and a multi-level marketing scam all rolled up into one.

The "last call" in a tavern is also a marketing opportunity. The customers may even load up on more drinks then they might otherwise order. After all, what the heck, it's... closing time.

and I lift my glass to the Awful Truth

which you can't reveal to the Ears of Youth

except to say it isn't worth a dime

And the whole damn place goes crazy twice

and it's once for the devil and once for Christ

but the Boss don't like these dizzy heights

we're busted in the blinding lights,

busted in the blinding lights

of CLOSING TIME

No need for jobs - everything's built!

…Gotta be stopped [this] working! ….. It’s made up by the ruling elite so we’re

tired and bored and can’t rebel and or philosophise about our own existence and

actually f..g evolve properly…

Says a particularly articulate non-working economist from Australia. Steve Hughes

Also: Steve Hughes on the Homeless

http://www.youtube.com/watch?v=Qm6kl17HH9s

Friday, November 8, 2013

Soaring Nominal Wages?

CNN/Money ran a story that makes me what to scream:

Over the last generation, pay for some professions has risen much faster than the overall rate of inflation.Since they do note consumer prices have increased from 1983 to 2012 (by a factor of 2.31), how hard it would have been for them to express these increases in real terms? I guess it is no surprise that the median wage for doctors have risen over the last 30 years – nominally by 276% but that represents a real increase of only 63%. OK, I have no pity for these impoverished doctors. But when CNN/Money tells us that some professions have seen wages rise by 170% - that’s also in nominal terms and represents only a 17% real increase. I’m glad that hotel clerks and firefighters haven’t suffered real wage erosion like some professions, but stories that tout the allegedly enormous increase in nominal salaries are just stupid.

Sunday, November 3, 2013

The Cooch May Win In VA

As of Friday, the Emerson poll shows Cuccinelli only 2 points behind McAuliffe. I fear my piece on short term memory may be too real. A week ago, MacAuliffe would have massively beaten Cuccinelli. Now the Cooch may win. He is running ads hard on the failed rollout of the Obamacare exchanges, which has totally dominated the news all week. No more government shutdown by Republican Tea Partiers in the public mind, now it is Obama incompetence, and the Cooch is running it hard. That ACA will probably get straightened out eventually does not matter. What matters is the perception right now, and that is not good for the Dems.

I also fear that all those polls showing Mac so far ahead may induce complacency, while the Cooch's supporters are fired up and have momentum. This is going to be very close in the end.

Oh, and of course this trend means that in the AG race Obenshain is probably well in the lead now, although I have seen no polls in the last few days on that one. Heck, Jackson might even pull through, although that still seems unlikely.

I also fear that all those polls showing Mac so far ahead may induce complacency, while the Cooch's supporters are fired up and have momentum. This is going to be very close in the end.

Oh, and of course this trend means that in the AG race Obenshain is probably well in the lead now, although I have seen no polls in the last few days on that one. Heck, Jackson might even pull through, although that still seems unlikely.

Subscribe to:

Posts (Atom)